Finding the best savings accounts retirees can rely on is essential for financial security. With a fixed income, retirees need a place to store their money that offers easy access, low fees, and a competitive interest rate. If you’re setting aside cash for everyday expenses, medical bills, or an emergency fund, the right savings account can help maximize your money’s potential.

High-yield savings accounts, credit union accounts, and money market options provide retirees with better interest rates than traditional savings accounts. Many online banks offer higher returns with fewer fees, making them attractive alternatives.

Below, you’ll compare the best retirement savings accounts based on interest rates, fees, and accessibility.

Best Savings Accounts for Retirees

The right savings account is crucial for retirees looking to maximize their financial security. High-yield savings accounts provide competitive interest rates, low fees, and easy fund management. Seeking flexibility, no minimum deposits, or a credit union option, retirees can choose from a range of savings accounts tailored to their needs.

Subscribe for free and get proven relocation and travel strategies, personalized support, valuable rewards, and trusted reviews for every move.

Your email has been added to our list.

These high-yield savings accounts are ideal for retirees –

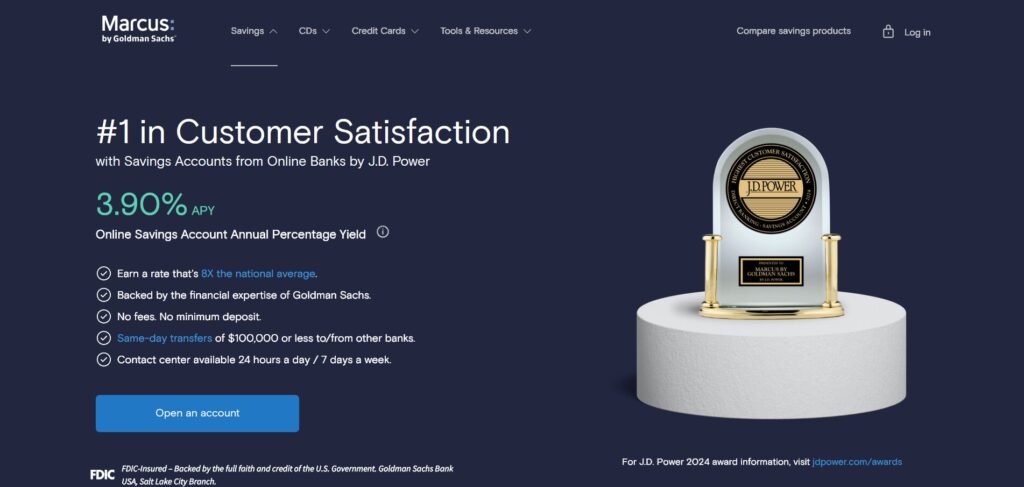

Marcus by Goldman Sachs High-Yield Savings

Best for – High interest rates with no fees

- APY – 4.40%

- Monthly fees – None

- Minimum deposit – None

- ATM access – No

Marcus by Goldman Sachs offers one of the highest APYs on the market, helping retirees grow their savings without taking risks. No monthly maintenance fees or minimum balance requirements make it easy to manage funds. However, this account lacks an ATM card, requiring withdrawals through a linked account.

Moreover, this account is ideal for retirees prioritising long-term savings over frequent withdrawals. Since it is an online-only bank, users benefit from competitive interest rates without the overhead costs associated with traditional banks. On the downside, those who prefer in-person banking services may find the lack of physical branches a disadvantage.

Strengths –

- It is one of the highest APYs on the market.

- There are no monthly maintenance fees or minimum balance requirements.

- A reliable option for retirees seeking stable returns.

Limitations –

- No ATM access for direct withdrawals.

- You must transfer funds to a linked account before using them.

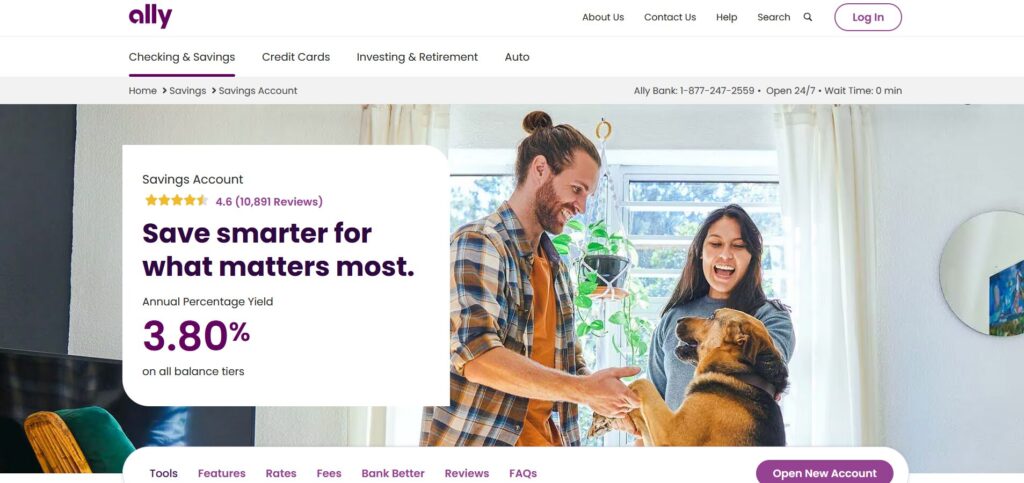

Ally Bank Online Savings

Best for – Retirees who want flexibility

- APY – 4.25%

- Monthly fees – None

- Minimum deposit – None

- ATM access – No

Ally Bank’s high-yield savings account provides a strong balance between growth and accessibility. It offers a competitive APY with no maintenance fees and allows retirees to set up savings “buckets” for different goals, such as medical expenses or travel. While there’s no ATM access, retirees can quickly transfer funds to an Ally checking account for withdrawals.

Besides, they provide a user-friendly mobile and online banking experience, making it easy to manage savings from anywhere. Since it operates entirely online, customers benefit from higher interest rates and lower fees than traditional banks. However, those who prefer in-person customer support may find the lack of physical branches a drawback.

Strengths –

- Competitive APY with no maintenance fees.

- It allows customizable savings “buckets” for different financial goals.

- Seamless transfers to an Ally checking account for easy withdrawals.

Limitations –

- No direct ATM access.

- Withdrawals require an external account transfer.

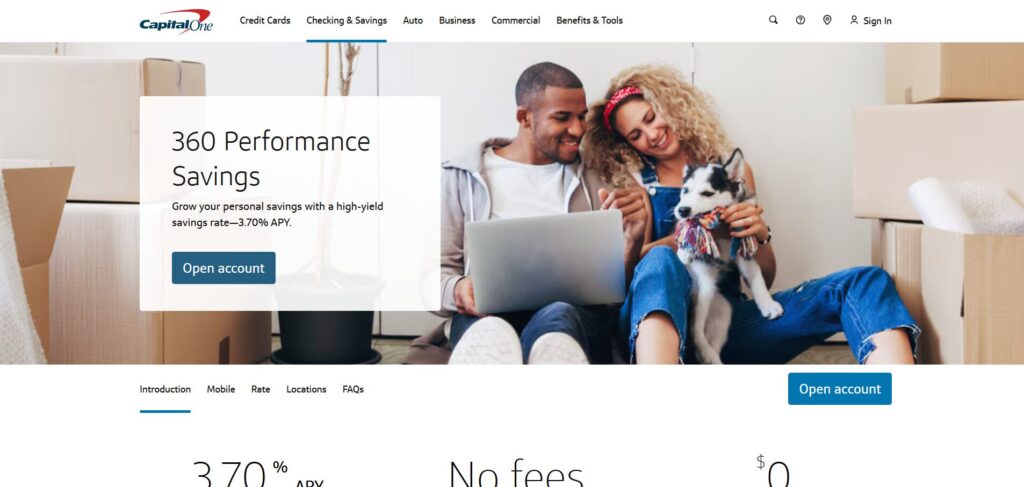

Capital One 360 Performance Savings

Best for – No minimum deposit requirements

- APY – 3.70%

- Monthly fees – None

- Minimum deposit – None

- ATM access – No

Capital One’s savings account is a strong option for retirees looking for a simple, high-interest account with no minimum deposit. The mobile banking app is easy to use, and there are no fees to worry about. However, like many online savings accounts, withdrawals must be transferred to a linked checking account.

Furthermore, it integrates well with other Capital One products, making it convenient for retirees who already have accounts with the bank. Because it offers strong digital banking tools, users can easily track savings, set up automatic transfers, and manage their money on the go. Still, those needing direct ATM access may find the transfer requirement inconvenient.

Strengths –

- No minimum deposit is required.

- Easy-to-use mobile banking app.

- No maintenance or hidden fees.

Limitations –

- No ATM card is available for cash withdrawals.

- Transfers to a linked checking account are necessary for access to funds.

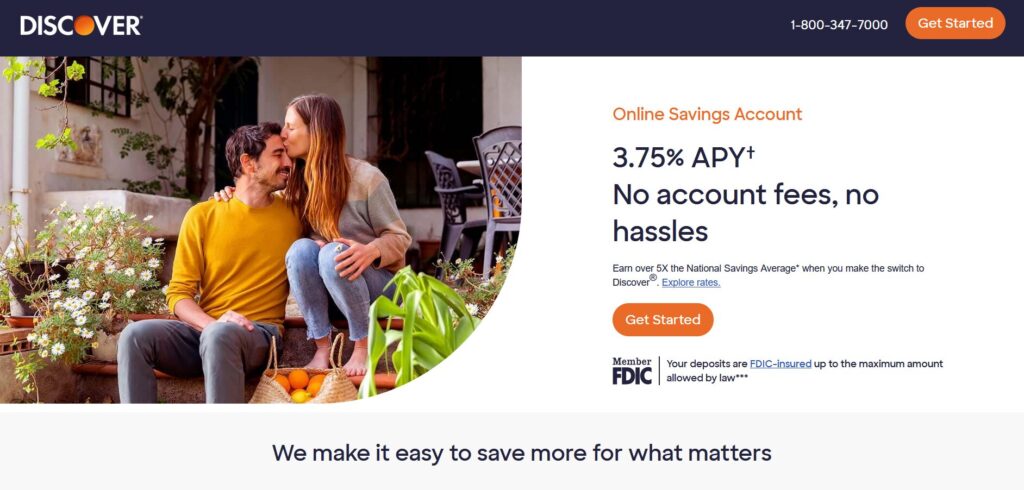

Discover Online Savings Account

Best for – A well-rounded online bank experience

- APY – 4.25%

- Monthly fees – None

- Minimum deposit – None

- ATM access – No

Discover’s online savings account offers a solid APY with no fees or minimum deposit requirements. The bank also provides a smooth online experience and strong customer support. However, as with most high-yield savings accounts, ATM withdrawals aren’t available. You need to transfer funds to a linked account before accessing cash.

Further, its online savings account includes a robust mobile app with advanced budgeting and tracking features. They allow retirees to monitor their savings effortlessly. Since it operates entirely online, customers benefit from competitive interest rates and a streamlined banking experience. However, those who prefer in-person service may find the lack of physical branches limiting.

Strengths –

- Strong customer support and user-friendly online banking.

- There are no fees or minimum deposit requirements.

- Competitive APY for long-term savings growth.

Limitations –

- No direct ATM access for withdrawals.

- You must transfer funds to a linked account before accessing cash.

Alliant Credit Union High-Rate Savings

Best for – Retirees who prefer credit unions

- APY – 3.10%

- Monthly fees – None with e-statements

- Minimum deposit – $5

- ATM access – Yes

Alliant Credit Union offers a high-rate savings account with decent APY and ATM access, a feature missing from many online banks. Retirees who prefer credit unions will appreciate the strong customer service and additional financial tools. Yet, the interest rate is lower than some online banks, and membership requirements apply.

Moreover, they provide a network of over 80,000 surcharge-free ATMs, making it easier for retirees to access cash when needed. Since it is a credit union, members may also qualify for lower loan rates and exclusive financial products that traditional banks may not offer. However, membership is limited, requiring retirees to meet criteria or donate to an affiliated organization.

Strengths –

- It provides ATM access, a feature missing from most high-yield savings accounts.

- Personalized customer service and strong financial tools.

- Credit union membership benefits.

Limitations –

- APY is lower than many online banks.

- Membership requirements apply, limiting access.

Subscribe for free and get proven relocation and travel strategies, personalized support, valuable rewards, and trusted reviews for every move.

Your email has been added to our list.

Alternatives to Traditional Savings Accounts for Retirees

Standard savings accounts offer security, but some retirees may seek higher returns or greater flexibility to better align with their financial goals. Money market accounts, certificates of deposit (CDs), and government-backed bonds provide alternative investment options for growing retirement funds while maintaining accessibility.

Look at these alternative savings options that offer retirees better yields and flexibility –

1. Money Market Accounts

Money market accounts (MMAs) offer competitive interest rates with check-writing privileges and debit card access. They work similarly to savings accounts but typically require a higher minimum balance. These accounts are ideal for retirees who want a mix of liquidity and stable returns. Many MMAs also come with FDIC insurance, ensuring added security for deposits.

Some top MMAs include –

- Sallie Mae Money Market Account (4.20% APY)

- CIT Bank Money Market (1.55% APY)

2. Certificates of Deposit (CDs)

CDs provide fixed interest rates for a set period, so they are ideal for retirees who don’t need immediate access to funds. Furthermore, longer-term CDs generally offer higher yields, but early withdrawals may result in penalties. Nevertheless, some banks also offer no-penalty CDs, allowing withdrawals without fees after a certain period.

Some of the best options include –

- Synchrony Bank 12-month CD (5.00% APY)

- Barclays 12-month CD (4.90% APY)

3. Treasury Bonds and I Bonds

Retirees seeking low-risk, inflation-protected savings may benefit from Treasury bonds or I Bonds. They offer a 5.27% APY and inflation protection, making them a strong savings alternative. In particular, bonds are especially valuable during high inflation, as their rates adjust every six months. On the other hand, Treasury bonds provide long-term stability and can be a valuable tool for estate planning.

4. Fixed Annuities

Fixed annuities provide retirees with a guaranteed income stream for years of life, offering stability and predictability. Unlike savings accounts, annuities lock in a fixed rate typically higher than standard savings rates. However, early withdrawals may incur penalties, and some annuities come with higher fees than traditional savings options. Fixed annuities offer retirees steady income and financial security.

?♀️ Also read – What Should be a Good Monthly Retirement Income?

Factors to Consider When Choosing a Savings Account

Selecting the right savings account is crucial for retirees who want to maximize returns, minimize fees, and maintain easy access to funds. While high-yield savings accounts offer competitive interest rates, other factors like withdrawal flexibility and bank reputation also play a significant role in financial security.

See some key factors to consider when choosing –

Interest Rate (APY)

A high annual percentage yield (APY) ensures savings grow over time. Traditional savings accounts often offer just 0.40% APY, losing value to inflation. Retirees should choose savings accounts with APYs above 4.00% to preserve purchasing power. High-yield savings accounts from Marcus by Goldman Sachs, Ally Bank, and Capital One 360 currently provide some of the most competitive rates.

Fees and Hidden Costs

Monthly maintenance fees, withdrawal fees, and excessive transaction penalties can quickly eat into savings. Moreover, many banks charge fees for not maintaining a minimum balance or exceeding the federal limit of six monthly withdrawals. Therefore, retirees should avoid accounts with unnecessary fees or look for institutions that offer fee waivers based on age, direct deposits, or maintaining a certain balance.

Withdrawal Flexibility

Some banks often limit how often you can withdraw money from savings accounts. Therefore, retirees who rely on their savings for daily expenses should choose an account that allows unlimited or frequent withdrawals without penalties. For example, credit unions and money market accounts typically provide easier withdrawal options than high-yield savings accounts that may limit transactions.

Bank Reputation and Security

A bank’s stability and reputation are crucial for retirees’ secure savings. Therefore, ensure that the institution is FDIC- or NCUA-insured, meaning deposits are protected up to $250,000 per account holder in case of bank failure. Besides, checking online customer reviews and customer service ratings can help retirees find a trustworthy financial institution that provides firm support when needed.

Online vs. Traditional Banking

Online banks typically offer higher interest rates. Yet, some retirees may prefer in-person banking for face-to-face financial advice, cashier transactions, or direct withdrawals. Those comfortable with digital banking can use higher APYs and lower fees at Discover, SoFi (read the complete review here), and American Express Savings.

However, retirees who need physical branches may opt for Chase, Wells Fargo, or local credit unions despite their lower APYs.

? Related – 15 Best Bank Accounts for Digital Nomads & International Travelers

Regularly Compare and Update Savings Accounts

Interest rates fluctuate due to economic conditions and Federal Reserve policy changes. Therefore, retirees should review savings account rates at least once a year to ensure they earn the best possible return. Additionally, some banks offer temporary promotional rates for new customers. As a result, it may be worthwhile to switch accounts if a significantly better APY becomes available.

Choosing the right savings account ensures retirees’ financial stability by maximizing interest, minimizing fees, and maintaining access. Keeping funds in a secure, high-yield, accessible account helps retirees maximize their savings. It also ensures they stay prepared for unexpected expenses.

How Interest Rates on Savings Accounts Affect Retirees

Interest rates significantly affect how much retirees can earn from their savings accounts. A higher annual percentage yield (APY) ensures that money grows steadily without requiring additional investment. However, savings account interest rates fluctuate based on economic conditions and Federal Reserve policies. Retirees benefit from better returns on high-yield savings accounts when interest rates rise.

Conversely, when rates drop, earnings decline, making it essential to compare options regularly. For retirees, the goal is to outpace inflation while maintaining easy access to funds. Purchasing power diminishes if a savings account’s APY is lower than the inflation rate. Retirees should consider diversifying their savings with money market accounts, certificates of deposit (CDs), or Treasury bonds.

Keeping an eye on the Federal Reserve’s interest rate changes can help retirees make informed decisions about where to store their cash. Banks and credit unions adjust APYs frequently, so switching to a better account when rates increase is a smart strategy.

Some banks offer promotional rates for new customers, which can provide an additional earnings boost. Retirees should review their accounts at least once a year to ensure they get the best possible savings returns.

Recommended read – How to Create a Retirement Budget

Subscribe for free and get proven relocation and travel strategies, personalized support, valuable rewards, and trusted reviews for every move.

Your email has been added to our list.

Why Liquidity Matters for Retiree Savings

Choosing a savings account requires considering liquidity and determining how easily you can access money without penalties. Unlike investments in stocks, real estate, or retirement accounts with withdrawal restrictions, liquid savings ensure that retirees have cash available for daily expenses, medical emergencies, or unexpected home repairs.

High-yield savings accounts balance liquidity and growth, allowing retirees to earn interest while keeping their money accessible. However, some accounts impose withdrawal limits, typically restricting account holders to six monthly withdrawals under federal regulations. Exceeding this limit may result in fees or account downgrades.

Retirees anticipating frequent withdrawals should, therefore, consider linking their savings account to a checking account for seamless transfers. Additionally, credit unions often offer flexible savings accounts with ATM access, which can be especially helpful for retirees who prefer withdrawing cash as needed.

Meanwhile, for those who don’t need daily access to all their funds, keeping a portion in a money market account or short-term CD can also provide higher yields while maintaining liquidity.

The key is balancing liquidity for emergencies and expenses while also earning the best interest on long-term savings. Additionally, reviewing financial needs and withdrawal habits helps retirees optimize savings and avoid unnecessary fees.

Frequently Asked Questions (FAQs)

1. What is the safest type of savings account for retirees?

High-yield savings accounts at FDIC- or NCUA-insured banks are the safest options. They ensure funds remain protected up to $250,000 per depositor.

2. Are high-yield savings accounts safe for retirement savings?

Yes, high-yield savings accounts offer better returns than traditional accounts while maintaining full liquidity and security.

3. How much should a retiree keep in savings?

Financial advisors recommend keeping six to twelve months’ living expenses in an easily accessible savings account.

4. Can retirees lose money in a savings account?

No, savings accounts at insured banks do not lose money. However, keeping too much in low-yield accounts can result in losing purchasing power due to inflation.

Sum It All Up

The best savings accounts retirees can use offer high interest rates, no fees, and easy access. Online banks typically provide the best returns, while credit unions offer personal service and ATM access. Retirees looking for alternatives may consider money market accounts, CDs, or Treasury bonds for better yields. By comparing rates and features, retirees can ensure their savings work for them.

It helps provide financial security and peace of mind throughout retirement.

Save More, Worry Less, and Move with Confidence with Us

Relo.AI simplifies finding and managing the best savings accounts retirees can rely on for financial stability.

If you’re looking for high-yield savings options, lower fees, or better accessibility, we provide expert insights and tailored recommendations to help you make informed financial decisions.

Also, if you’re planning a retirement relocation, we offer seamless support to help you quickly move to a new city or country.

Get expert advice by booking your FREE consultation and retire with confidence.