You may be paying too much to live when housing and fixed location costs consume over half of your take-home pay. At that point, savings flatten, and options begin to narrow. When rent, taxes, utilities, and transportation rise faster than income, even strong salaries lose force. The warning sign rarely appears as a single bill. It shows up in the trend line.

Over time, this imbalance changes how people make money decisions. Spending becomes cautious, planning shortens, and choices turn reactive.

Keep reading to see how everyday expenses can quietly drift out of balance with income and future flexibility.

Why This Matters Now for Many Households

In recent years, the American housing market has slipped into a new normal that feels familiar. Daily routines continue, bills get paid, and households expect next month to bring relief. Over time, the shift becomes evident. The bill stack has grown taller.

Subscribe for free and get proven relocation and travel strategies, personalized support, valuable rewards, and trusted reviews for every move.

Your email has been added to our list.

The data confirms the pressure. In 2023, the Census Bureau reported that over 21 million renter households were above the standard affordability threshold. At the same time, Harvard’s Joint Center for Housing Studies has tracked the pressure building year after year, with cost burdens setting records and repeating.

Meanwhile, rents remain elevated. Redfin data shows asking rents continuing to rise, even as the pace shifts by month and metro. This matters because households rarely budget for volatility. A lease renewal hits, taxes adjust upward, insurance premiums increase, and location costs stop feeling temporary.

As a result, when paying too much to live, they often blame themselves first. They assume a missed promotion, weak savings, or careless spending. In reality, the pattern frequently begins with geography. Urban cost pressure can make even careful households feel careless.

Related – Geographic Arbitrage: Earn More By Living Where Costs Are Lower

How Much Is Too Much to Sustain

Benchmarks are imperfect, but they help separate discomfort from imbalance.

A household typically enters cost-burdened territory once housing costs exceed 30% of income. This standard, widely used in research and policy, including by HUD and Harvard’s housing research, provides a baseline. Beyond that, a severe cost burden is often discussed when housing consumes 50% or more.

In practical decision making, a location can start to look risky when these thresholds occur together –

- First, housing exceeds 30 to 35% of gross income

- Housing plus utilities and insurance exceeds 40%

- Housing plus all fixed location costs approaches or exceeds 50%

At the same time, transportation costs remain high because the location requires a car or a long commute.

Notably, transportation is frequently the hidden accomplice. According to AAA’s annual analysis, the cost of owning and operating a new vehicle reached $11,577 per year in its 2025 report, close to $965 per month.

Importantly, the point is not that every household owns a new car. Rather, the point is that location-driven transport costs can rival a second rent payment.

Ultimately, when you are paying too much to live, the budget does not collapse in one dramatic moment. Instead, it tightens. Gradually, it begins to refuse new goals.

Signs You Are Paying Too Much to Live

Cost pressure rarely announces itself directly. Bills arrive on schedule. Income appears stable. Over time, tradeoffs increase, and flexibility fades. As a result, many households begin to sense that location costs no longer match what they receive in return.

Common signs include –

1. Housing costs exceed sustainable limits

If housing costs keep rising while income stays steady, the location begins to set your ceiling. In that case, this becomes the classic burden problem, and in many markets, it is widespread. As a result, each increase reduces your ability to absorb a job change, a medical bill, or a family need without relying on debt.

2. Income growth no longer improves your daily life

A raise arrives and, almost immediately, disappears into rent, taxes, and insurance. As a result, nothing feels lighter. The implication, then, is that the location has become a tax on ambition. In practice, you work harder to stand in the same place.

3. You rely on short-term coping tools

Some households begin splitting rent across paychecks or using payment products to manage timing. At the same time, news reporting has shown renters turning to “rent now, pay later” services, which, in turn, can add fees and amplify financial strain (APN News).

4. Your savings rate has stopped moving

You still save, but the number stays flat. Over time, emergency funds plateau. Meanwhile, retirement contributions freeze at the same level year after year. Taken together, the implication is that you are paying too much to live relative to a long horizon, even if bills continue to get paid.

5. You postpone life decisions because the math looks fragile

Family planning, career pivots, education goals, and even necessary repairs begin to feel risky. Ultimately, the implication is that the location is shaping choices that should belong to you.

6. You trade health and time for rent

Long commutes, second jobs, and side hustles begin to crowd out rest. The location requires constant output simply to remain. The implication, however, is not only financial. At a physiological level, chronic cost pressure pushes stress into the body.

7. The home itself keeps asking for money

For owners, maintenance, repairs, rising insurance, and property tax creep are rarely stable. At the same time, Harvard has reported increases in homeowner cost burdens in recent years, driven by expenses that rise beyond the mortgage payment. Ownership can become a drag when the total cost line grows faster than income.

Also read – The Ultimate Relocating Checklist for a Smooth and Organized Relocation

Property Cost Breakdown You Can Actually Use

Too often, many budgets fail because they treat housing as one number. In reality, housing functions as a system. Each component moves at a different pace, and increases rarely arrive together. Over time, small adjustments compound into meaningful pressure.

Below, a simple way appears to map true monthly costs. Use it whether you rent or own –

| Cost category | Renting | Owning |

| Base payment | Rent | Mortgage principal and interest |

| Utilities | Electric, gas, water, and internet | Same, often higher for a larger space |

| Insurance | Renter insurance | Homeowners insurance plus rising premiums |

| Taxes and fees | Often embedded | Property tax, HOA, special assessments |

| Maintenance | Usually limited | Repairs, upkeep, replacements |

| Mobility cost | Lease break or moving cost | Selling costs, time on market, refinance risk |

Owners sometimes underestimate the “ownership drag.” In practice, this includes time, administrative work, and unpredictable repairs. Meanwhile, renters sometimes underestimate rent volatility. This is especially true in markets where new lease prices reset quickly.

When a household is paying too much to live, the mistake is not renting or owning. The mistake is failing to track the full stack.

Comparison Snapshot

Cost differences often remain abstract until they are placed side by side. Numbers feel manageable in isolation. Patterns emerge only when expenses are viewed together. Over time, comparisons clarify which costs are structural and which are optional. Households begin to see how location shapes outcomes more than effort alone.

Consider a professional household with two different scenarios –

Scenario A

A high-cost metro area sets the baseline. Here, housing plus utilities consume about 45% of take-home pay. At the same time, transportation requires a car and adds a significant monthly bill. As a result, savings rise slowly.

Scenario B

A mid-cost market changes the equation. In this setting, housing plus utilities consume closer to 30%. Shorter commutes cut transportation spending. Savings build faster.

Importantly, this is not a theory. Broad measures of rent burden show many renters spending over a third of their income on rent across large parts of the country (People). In practice, the difference in outcomes often comes from fixed costs, not spending discipline.

The Emotional Toll of Paying Too Much to Live Over Time

People rarely discuss the psychological dimension with precision, yet it has a shape. When you are paying too much to live, you begin to make decisions with a short horizon. Over time, caution grows without clarity. Delayed expenses incur higher costs. In parallel, you accept job conditions you might otherwise refuse. Over time, you treat movement as impossible, even when it is only difficult.

At the same time, the pressure narrows imagination. Instead of planning around goals, a household starts to plan around constraints. That shift, while subtle, marks the difference between living with agency and living with compliance.

Subscribe for free and get proven relocation and travel strategies, personalized support, valuable rewards, and trusted reviews for every move.

Your email has been added to our list.

For this reason, a calm tone matters. Panic rarely helps. Importantly, this is not a moral failure. Rather, it is a structural problem that households can measure.

What People Usually Miss When Paying Too Much to Live

Cost pressure rarely looks dramatic from the inside. Daily routines continue. Familiar choices repeat. Over time, habits begin to replace analysis. Many households overlook the forces that quietly lock them into high-cost locations.

Common patterns include –

Sunk cost thinking

Staying longer increases the friction of leaving. Gradually, the time invested turns into a reason to remain. Yet, sunk costs reflect history, not strategy.

Identity tied to location

Some cities function as a badge. As a result, leaving can feel like losing status. That emotion, while real, can become expensive.

Social pressure

Friends normalize the same burden. Because everyone pays too much, it feels acceptable. However, shared pain does not make the math sustainable.

The illusion of stability

Renters assume a lease is stable until renewal. Similarly, owners assume equity serves as a safety net until a major repair or tax increase arrives. In reality, housing stability can exist, but it must be earned with margin.

Ultimately, when households pay too much to live, what they miss is margin. And, margin remains the whole point.

When Paying More Makes Sense

A fair article has to say this clearly. Paying more can be rational. It can support career growth, family needs, or access to specific opportunities. The problem begins when higher costs cease to be intentional and become permanent.

It can make sense when –

- The location produces real career leverage and network access

- The arrangement is time-bound, with an exit plan

- Income growth is likely to outpace housing costs

- The household is building skills or credentials that raise future earning power

- The household can maintain savings while paying the premium

The test is whether the premium yields measurable benefits. If it buys only familiarity, then you may be paying too much to live for comfort that no longer protects you.

Recommended read – New Bilt Card 2.0 Arrives With a New Take on Housing Rewards

A Decision Framework to Identify Paying Too Much to Live

Use this as a quarterly check. Put it on paper. To stay grounded in reality, review it alongside bank statements, housing bills, and savings data.

Trends matter more than one-month snapshots –

- Income trend – Is income rising, flat, or uncertain over the next 12 months?

- Fixed cost trend – Have housing, taxes, insurance, utilities, and transport risen faster than income?

- Savings trend – Is your savings rate increasing, stable, or declining? Track it as a percentage, not only as a number.

- Optionality – If you lost income for 60 days, could you stay without debt? If you needed to relocate for a better role, could you move?

- Exit friction – How hard is it to change course? Consider lease penalties, selling costs, school timing, and work constraints.

If three or more answers show declining flexibility, you are likely paying too much to live for the outcomes you want.

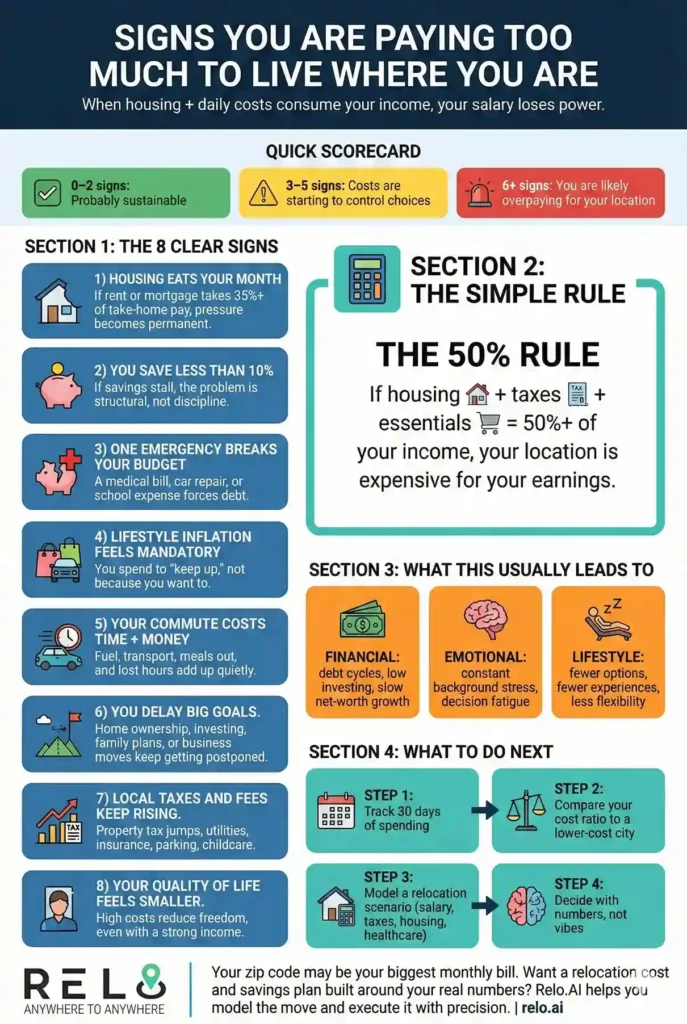

A Visual Scorecard for Location Cost Pressure (PDF)

Living costs rarely signal trouble all at once. In practice, this visual scorecard maps the financial, emotional, and lifestyle indicators that reveal when a location begins to work against income rather than support it.

The scorecard breaks down housing, taxes, transportation, and daily expenses into clear thresholds, showing how cost pressure builds gradually and why strong salaries can still lose impact. Each section reflects common, measurable patterns households experience before flexibility disappears.

Subscribe for free and get proven relocation and travel strategies, personalized support, valuable rewards, and trusted reviews for every move.

Your email has been added to our list.

Designed for renters and homeowners evaluating whether their location still makes sense, this graphic helps translate abstract cost stress into concrete signals that are easy to assess.

Download Now (High-Quality PDF Version)

Frequently Asked Questions (FAQ) About Paying Too Much to Live

1. What percentage of income should go to housing?

Many researchers and policymakers use 30% as a key affordability threshold, and burdens rise sharply beyond that (huduser.gov).

2. How do you know if your problem is the house or the city?

Compare your fixed costs to a second market using the same income. If the difference materially changes savings and optionality, geography is a major factor.

3. Can owning a home still be a burden even if prices rise?

Yes. Many homeowners see equity increase. Ongoing costs continue to push total housing expenses higher.

A Structured Way to Lower Living Costs Without Disruption

Relo.AI helps households step back from rising location costs and make informed, deliberate decisions. Through structured cost analysis, housing review, and long-term planning, we pinpoint where fixed expenses can decrease without disrupting stability, work, or daily life.

We manage the full relocation process. This includes comparing alternative cities or countries and coordinating housing, logistics, and timing.

For those questioning if their current location still makes financial sense, clarity often changes everything.

Schedule a FREE call with us to understand how paying less and relocating strategically can restore flexibility and help you live more freely.

Wrapping Up!

If you suspect you are paying too much to live, the next step is not a dramatic move. The next step is to inventory fixed costs and trends clearly. A household can tolerate high costs during a strategic phase. It cannot tolerate permanent cost creep without losing freedom. A household can absorb high expenses during a defined period. It struggles when temporary pressure turns into permanent cost creep, quietly limiting choice and financial freedom.

The goal is control over long-term outcomes.